Open APIs in Jordan Where Does the Jordanian Financial System Stand On Open APIs?

The evolution of banking shows a gradual shift from the analog to the digital with almost all advances in retail banking within the past century or two owe their existence to a leap forward in technology. Innovative financial technology, however, is radically changing the financial services landscape. Digital economies are now emerging from revolutionary digital financial services, which are experiencing an unprecedented velocity of technological developments.

A hallmark of this took place in Berlin following TESOBE’s CEO Simon Redfern’s establishment of The Open Bank Project (OBP) In 2010. At its core, OBP is an open-source initiative to “define a set of data access and API standards that would facilitate public and authorized access, searching and crosslinking of financial transactions”.

Open Banking enables individual customers and businesses to freely mobilize their financial and or non-financial data across third parties, an effort that challenged the banking industry’s predominantly defensive and possessive approach to managing customers’ data and their financial transactions. Fintech firms’ persistence, often through the use of riskier measures such as screen scraping when their request for access is not granted by banks, has led to fierce competition and heightened risks from Fintech firms, as well as higher rates of customer churn in plight of more holistic, convenient financial services.

Luckily, this inhibitory trend is winding down globally, as banks are beginning to realize the importance of collaboration with Fintech firms to extend the sector’s capacity to innovate through enabling access to their own APIs securely while maintaining their own customer base.

On this account, Financial Regulators are faced with the potential of assuming an exciting, critical new role in supporting and incubating the appropriate market conditions for Open Banking. The maturity of technology and data-driven business models have become universally apparent to Financial Regulators, and the need for data-driven regulation to enable wider sector reform.

This has led to versatile approaches taken by regulatory and authoritative bodies in enabling Open Banking. The boldest of which was the UK’s Competition and Markets Authority setting up the Open Banking Initiative in 2014 to increase competition and innovation in financial services. This was followed by the launch of the European Union’s Second Payment Services Directive (PSD2) and the UK’s own Open Banking Standards promising to drive innovation in banking and payment services, by making it easier for customers, banks and other third-party service providers to securely share data with each other and capitalize on the opportunity.

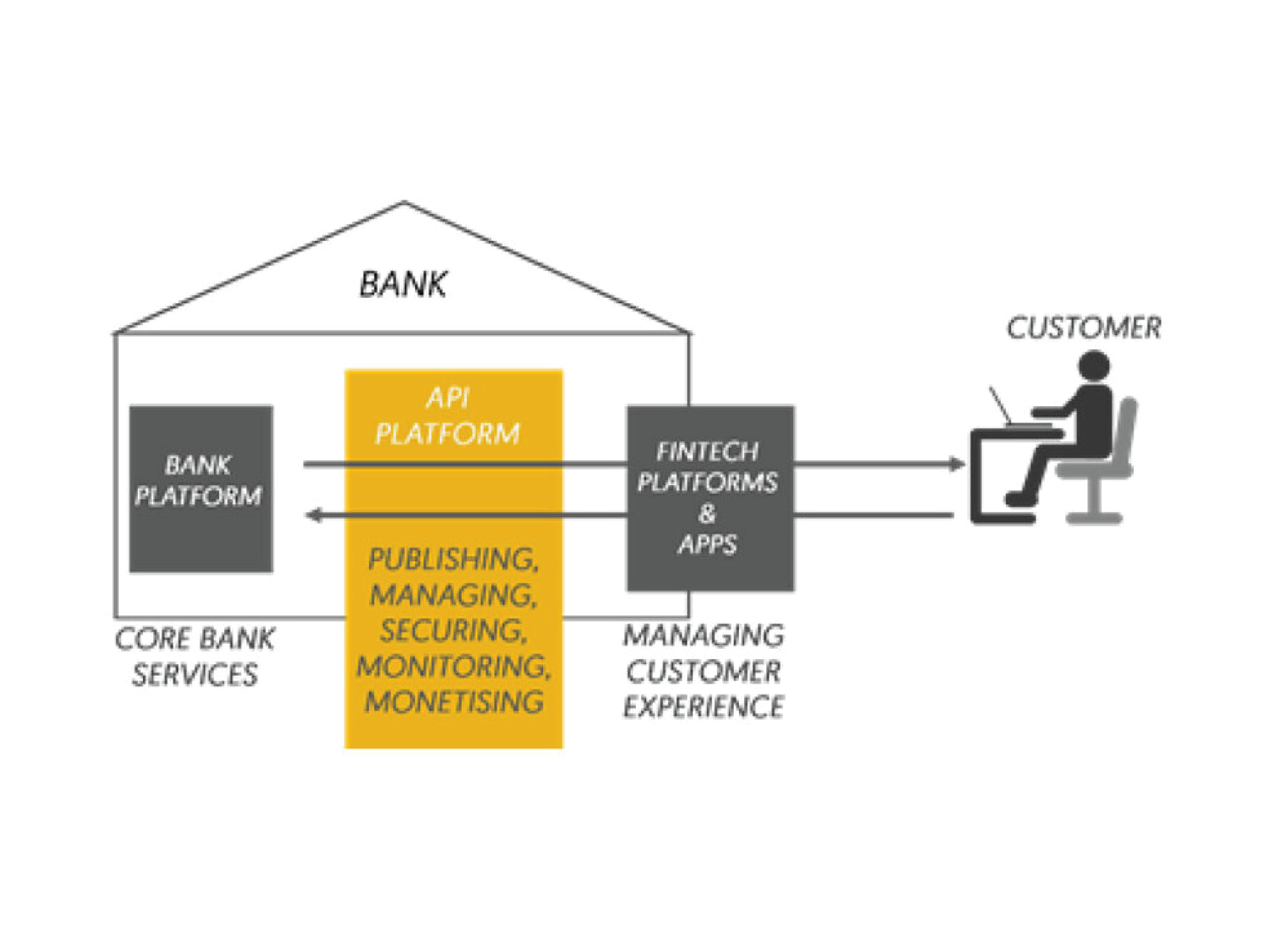

According to Investopedia, Open Banking is a system that provides a user with a network of financial institutions’ data using application programming interfaces (APIs). By opening APIs to sharing, third parties have easier access to financial information, which allows them to build new and different apps and services.

APIs simply allow the sharing of information between systems, while Open APIs refer to a publicly available interface that gives access to the sharing of data or functionality. In open banking, open APIs give third parties access to a financial institution’s customer data (with the customer’s permission) or to the financial institution’s service offerings and their functionality. This is important because it can allow customers to have better control over their own data and gives third parties the ability to create value-added services for customers.

In particular, Open APIs have started with payment services in most jurisdictions, then went beyond to encompass lending products, Personal Financial Management (PFM) products with further potential for scalability of other digital financial services. Internationally, Open Banking has flourished in jurisdictions with existing personal data protection regulations and policies (GDPR in Europe or Consumer Data Rights in Australia).

Open Banking vs. Open APIs: The phenomena and the underlying technology

With necessary country-specific contextualization, more and more countries are joining the open banking movement, including some in the MENA region, which brings us to our focal question of the readiness of the Jordanian banking sector to provide open APIs, and the Central Bank of Jordan’s position towards open banking.

Jordan

Banks opening their specific APIs is not new in Jordan. Our Jordanian banks have adopted it with card processors, ATM processors, and the EBPP System (eFAWATEERcom) . However, their approach required third parties and fintechs to go into a cumbersome process to get the approvals, to sign bilateral contracts, to go into harsh negotiations and individual integrations, etc.

Open APIs simplify these processes regardless of the parties involved, thereby eliminating the need for extra procedures or costly approvals that need to be done individually.

We heard H.E. the Governor of the CBJ on several occasions discussing open APIs in the area of digital payments, as a stepping stone towards open banking in the kingdom; as part of H.E.’s sincere endeavor to encourage the FinTech ecosystem in the kingdom.

So which approach is the CBJ going to adopt? A mandatory or voluntary regime? Would the CBJ follow a market-driven approach with guidelines and encouragement, or would they instead legislate? Would it be standardized or non-standardized? Would the CBJ exclusively target the largest banks or a certain number of banks?

Open Banking Regulatory Models

There are currently four approaches to Open Banking:

The Commander Approach (Mandated and standardized): the regulator provides the legal and security framework as well as the technical interfaces, which are standardized across banks, and mandates adoption of said frameworks and interfaces; e.g. UK, Australia, Mexico

The Architect Approach (Mandated and non-standardized): the regulator provides the legal and security framework for the regime but not the technical interfaces, and mandates the adoption of said frameworks; e.g. EU, Japan

The Advocate Approach (market-driven and standardized): the industry provides a standard which is offered for voluntary adoption; e.g. New Zealand, Malaysia, USA

The Diplomat Approach (market-driven and non-standardized): the regulator provides information and guidelines for banks wanting to adopt Open Banking on a voluntary basis; e.g. Singapore, Hong Kong

As is the case with everything, there is no one-size-fits-all approach. The CBJ must weigh varying factors in planning its approach towards the adoption of open banking that best fits the Jordanian market, while maintaining its top priority of regulatory oversight and risk management.

During a workshop conducted by JoPACC for all commercial banks at the Banks’ Association of Jordan in May 2019, our guest speakers and panelists asked JoPACC to invite the sector to brainstorm and discuss the topic and to establish a task force to propose open banking guidelines suitable for the Jordanian market to be communicated with the CBJ.

Accordingly, JoPACC is conducting a sector-wide survey to analyze and report on the Sector’s readiness for Digital Transformation in preparation for a sector seminar to prepare for open banking. JoPACC is also studying the potential for having an API gateway for its instant payment system (IPS) to enable licensed third parties to provide innovative payment solutions that serve banks’ customers.

Jordan is well-positioned to be a leader and champion of Open Banking in the region. With the progressive vision of its Central Bank, evident eagerness of its financial sector, and superb maturity of the financial rails supporting its financial sector, all that is missing is a collaborative, courageous step into the future of banking.

JoPACC in particular is thrilled to be part of such a dynamic and collective drive to revolutionize the experience of customers across the kingdom, and the value they derive from the available financial services and is willing to be a facilitator and a leader in achieving this vision for Jordan.

Written by

Maha Bahou

Explore More Blog Posts

See All Blog Posts